With increasing globalization, many Non-Resident Indians (NRIs) are looking to invest in India, especially in real estate. One of the most popular methods for NRIs to purchase property is through home loans offered by various banks in India. However, the process of securing a home loan for NRIs is slightly different from that for residents. This blog will walk you through everything you need to know about NRI home loans, including document checklists, the best banks, differences between NRI and normal home loans, and more.

What is an NRI Home Loan, and Who Can Apply?

Image: HDFC

An NRI home loan is a specialized loan product tailored for Non-Resident Indians who wish to buy property in India. These loans cater to the needs of NRIs who are either salaried or self-employed abroad. NRIs can purchase new homes, construct a house on a plot, or even renovate an existing property with these loans. The eligibility criteria generally depend on the country of residence, age, income, and other factors. Also Read Income Tax Rules for NRIs Buying Property In India.

Why Do NRIs Prefer Home Loans for Property Investment in India?

NRIs prefer home loans for several reasons. First, home loans provide financial leverage, allowing NRIs to invest in premium properties without using all their savings. Secondly, NRIs enjoy tax benefits under Section 80C of the Income Tax Act. Thirdly, taking a home loan helps maintain a credit score in India, which can be beneficial for future investments. Also Read about Income Tax Rules 2024 for NRIs Selling Property in India

What Documents are Required for NRI Home Loans?

Understanding the document requirements is crucial for NRIs applying for a home loan. Below is a comprehensive checklist of documents required by most Indian banks.

- Identity Proof: Passport and visa copies.

- Address Proof: Overseas address proof (utility bills, driving license).

- Employment Proof: Offer letter, employment contract, and work permit.

- Income Proof: Last three months’ salary slips, six months’ overseas bank statement, and six months’ NRE/NRO account statement in India.

- Property Documents: Sale agreement, property title deed, and other relevant property documents.

- Power of Attorney (PoA): This is usually required if the NRI is not present in India for signing the loan agreement.

- Credit Score Report: A credit report from the country of residence, if available.

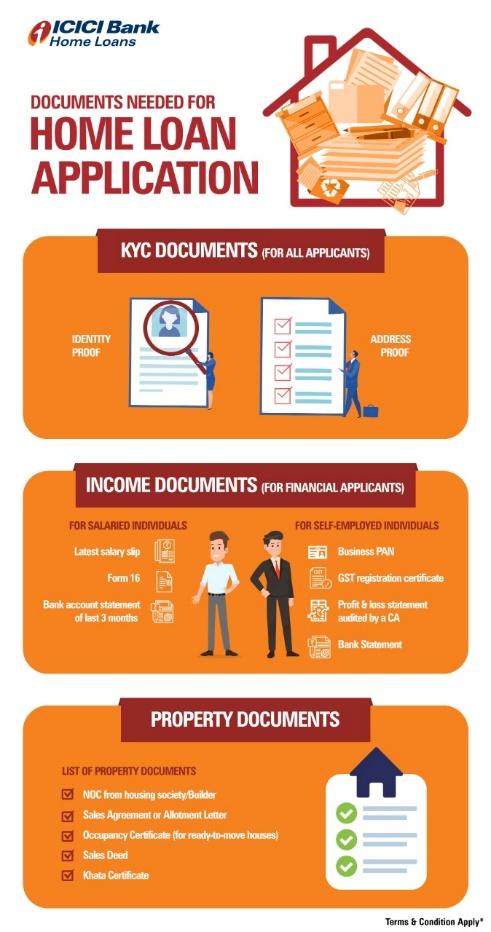

What Are the NRI Home Loan Documents Required by ICICI?

ICICI Bank is a popular choice among NRIs due to its competitive interest rates and seamless loan processing. Below are the specific documents required for an NRI home loan from ICICI:

- Passport and Visa: Mandatory for all applicants.

- Employment Proof: Offer letter and recent employment contract.

- Income Proof: Latest three months’ salary slips, six months’ bank statements, and Form 16 or the latest ITR.

- Power of Attorney: Must be executed in ICICI’s format and notarized.

- Property Documents: Title deed, sale agreement, and property tax receipts.

- NRI Status Proof: Valid visa or work permit.

What is the ICICI NRI Home Loan Interest Rate?

The interest rate for NRI home loans varies depending on factors such as the loan amount, tenure, and applicant profile. As of now, ICICI Bank offers competitive rates for NRI home loans, which generally range between 8.25% to 10.00%. The rate is subject to change, so it’s advisable to check ICICI’s official website or contact a loan officer for the latest rates.

How is an NRI Home Loan Different from a Normal Home Loan?

When comparing NRI home loans with normal home loans, several differences arise, primarily in eligibility criteria, documentation, and interest rates.

- Eligibility Criteria: NRIs must have been working abroad for at least a year, while resident Indians don’t have such criteria.

- Income Proof: NRIs need to provide overseas income proof, whereas residents provide Indian salary slips or income documents.

- Power of Attorney: NRIs need a PoA if they can’t be present in India for document signing, unlike resident Indians.

- Interest Rates: NRI home loans may have slightly higher interest rates compared to resident home loans due to perceived risk factors.

Which Banks in India Offer the Best NRI Home Loans?

Several Indian banks offer NRI home loans with varying terms and conditions. Some of the top banks include:

- ICICI Bank: Known for its flexible loan tenures and competitive interest rates.

- HDFC Bank: Offers a wide range of loan products with minimal paperwork.

- State Bank of India (SBI): Provides attractive interest rates and higher loan amounts.

- Axis Bank: Offers quick loan approvals and customer-friendly policies.

What Are the Benefits of NRI Home Loans?

NRI home loans come with numerous benefits, making them an attractive option for overseas Indians. Some of these benefits include:

- Financial Leverage: Allows NRIs to invest in high-value properties without depleting savings.

- Tax Benefits: NRIs can claim tax deductions on principal repayment and interest payments under the Indian Income Tax Act.

- Property Management: Many banks offer property advisory services, assisting NRIs in managing their investments in India.

How Does the Application Process for an NRI Home Loan Work?

Image: ICICI Bank

Applying for an NRI home loan involves several steps:

- Eligibility Check: Determine if you meet the basic eligibility criteria set by the bank.

- Documentation: Gather all necessary documents as per the bank’s requirements.

- Application Submission: Submit the application online or through a designated representative in India.

- Verification: The bank verifies the documents and assesses the applicant’s creditworthiness.

- Sanction: Upon successful verification, the loan is sanctioned, and a sanction letter is issued.

- Disbursement: The loan amount is disbursed either in a lump sum or in tranches, depending on the property purchase stage.

What Factors Should NRIs Consider When Taking a Home Loan?

While taking an NRI home loan, consider the following:

- Interest Rates: Compare interest rates across banks to find the most affordable option.

- Loan Tenure: Opt for a tenure that balances EMI affordability and total interest payout.

- Processing Fees: Look for hidden charges such as processing fees, legal fees, and prepayment penalties.

- Repayment Options: NRIs can repay their home loans through NRE or NRO accounts. Some banks also allow repayment through inward remittances.

Can NRIs Buy Any Type of Property with a Home Loan?

NRIs can buy most types of properties in India, such as residential apartments, bungalows, and plots. However, agricultural land, plantation properties, and farmhouses are restricted unless inherited or gifted.

How to Improve Your Chances of NRI Home Loan Approval?

To improve your chances of loan approval, maintain a strong credit history in your country of residence, ensure accurate documentation, and keep all property-related paperwork ready. Having a reliable Power of Attorney in India can also facilitate a smoother process.

Conclusion

NRI home loans are an excellent opportunity for overseas Indians to invest in the burgeoning Indian real estate market. By understanding the documentation requirements, interest rates, and other nuances of NRI home loans, you can make an informed decision that aligns with your financial goals. Whether you are looking to buy a luxury apartment or a serene villa, the right home loan can turn your dreams into reality. Also Read Real Estate Growth in India Over the Last 10 Years and Future Prospects

At Housiey, we aim to simplify your real estate journey, whether you’re an NRI or resident. Our platform connects you with the best properties in prime locations, ensuring you make the most of your investment. Let us help you find your dream home today!

FAQs

1. What is an NRI home loan?

- An NRI home loan is a financial product offered to Non-Resident Indians to purchase, construct, or renovate property in India.

2. What documents are required for NRI home loans?

- Common documents include identity proof, overseas address proof, employment and income proof, property-related documents, and a Power of Attorney.

3. Do NRI home loans have higher interest rates than normal home loans?

- Yes, NRI home loans often have slightly higher interest rates due to perceived risks associated with overseas borrowers.

4. Can NRIs buy agricultural land with a home loan?

- No, NRIs are restricted from purchasing agricultural land, plantation properties, or farmhouses unless inherited or gifted.

5. What is the ICICI NRI home loan interest rate?

- The interest rate typically ranges from 8.25% to 10.00%, varying based on the loan amount, tenure, and applicant’s profile.

6. Is a Power of Attorney mandatory for NRI home loans?

- Yes, a Power of Attorney is mandatory if the NRI is unable to be present in India for signing the loan agreement.

7. Can NRIs claim tax benefits on home loans in India?

- Yes, NRIs can claim tax benefits on principal and interest repayment under Section 80C and Section 24(b) of the Income Tax Act.

8. What is the maximum tenure for NRI home loans?

- Most banks offer a maximum tenure of up to 20 years, though it can vary depending on the bank’s policy and the applicant’s age.

9. Can NRIs repay home loans through foreign currency?

- No, repayments must be made through NRE, NRO, or FCNR accounts in India or through inward remittances in Indian Rupees.

10. Which banks offer the best NRI home loans?

- ICICI, HDFC, SBI, and Axis Bank are among the top banks offering competitive NRI home loans.

11. Are there any hidden charges in NRI home loans?

- Hidden charges may include processing fees, administrative charges, legal fees, and prepayment penalties, depending on the bank.

12. How does ICICI differ from other banks in NRI home loans?

- ICICI is known for its flexible loan tenures, easy documentation process, and personalized services for NRIs.

13. Can NRIs get a home loan for property renovation?

- Yes, NRIs can avail of home loans for renovation, repair, and extension of existing properties.

14. What happens if an NRI defaults on a home loan?

- The bank may seize the property and auction it to recover the outstanding loan amount.

15. How can NRIs improve their credit score in India?

- Maintaining timely EMI repayments, reducing outstanding debt, and keeping a healthy credit history in India can improve scores.

16. Can NRIs apply for joint home loans?

- Yes, NRIs can apply for joint home loans with close family members, such as a spouse or parents residing in India.

17. What is the role of a co-applicant in NRI home loans?

- A co-applicant shares the responsibility of repaying the loan, which can enhance loan eligibility and ease repayment burdens.

18. Can NRIs prepay their home loans?

- Yes, NRIs can prepay their loans fully or partially, though some banks might levy prepayment charges.

19. Are there any restrictions on the loan amount for NRIs?

- The loan amount depends on the NRI’s income, repayment capacity, and the specific bank’s policies; some banks may cap the amount based on risk factors.

20. What is the processing time for NRI home loans?

- The processing time is typically between 15 to 30 days, influenced by the completeness of documentation and speed of verification.

Also Read about Upcoming new airports in india

Post navigation

Previous Post

Michael Clark wins hero world hard Dirt Race10

Michael Clark wins hero world hard Dirt Race10