Introduction: Understanding Home Loan Foreclosure

Home loan foreclosure, also known as prepayment, refers to the process of closing a home loan by paying off the entire remaining principal amount before the original loan tenure ends. This option can help borrowers save significantly on interest costs, making it an appealing choice for those with excess funds or improved cash flow. However, foreclosure isn’t a simple decision—it involves charges, regulatory guidelines, and potential impacts on tax benefits. This guide explores everything you need to know about home loan foreclosure, including charges, types, RBI guidelines, benefits, and potential drawbacks.

What is Home Loan Foreclosure?

Home loan foreclosure essentially means terminating a loan agreement early by paying the outstanding balance in one lump sum. For borrowers who have taken a substantial loan with a long tenure, foreclosure can lead to considerable savings on interest. However, banks and lending institutions often levy foreclosure charges to compensate for the interest income they lose when borrowers repay early. These charges vary based on factors like loan type, rate (fixed or floating), and borrower profile.

Foreclosure may not always be a straightforward choice, as it can impact liquidity, tax benefits, and credit profiles. Thus, evaluating its pros and cons within the context of personal financial goals is essential for borrowers.

If you’re seeking alternative ways to manage your loan burden without foreclosing, check out our blog on “Reduce Your Home Loan Tenure – 5 Validated Tactics.”

Types of Home Loan Closure: What Are the Options?

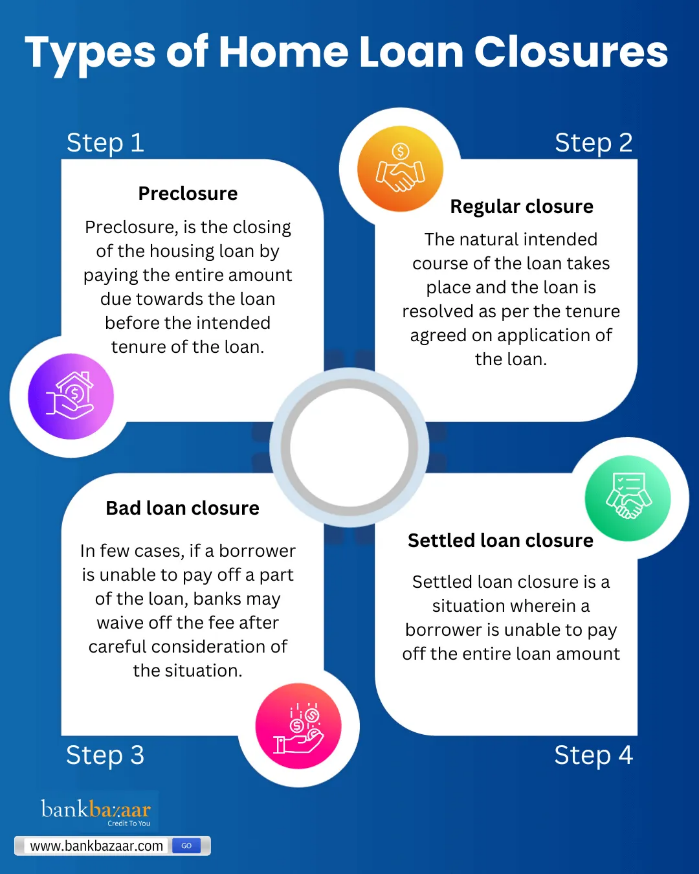

- Preclosure

Preclosure occurs when a borrower chooses to repay the outstanding principal ahead of schedule. This type of foreclosure is popular with those who’ve received a sudden windfall (e.g., a bonus, inheritance) or have saved up over time. Preclosure is advantageous for borrowers on high-interest loans, as it curtails long-term interest payments. However, it may attract a foreclosure charge, depending on the lender and loan terms. - Regular Closure

A regular closure is the planned end of a loan, occurring when the borrower pays the EMIs for the full loan term as initially agreed. It doesn’t involve any additional charges, and the borrower can retain all applicable tax benefits until the end of the loan. Regular closure is the natural course for most home loans, where EMIs continue until the tenure’s end. - Bad Loan Closure

Bad loan closure may arise when a borrower cannot fulfill the loan obligation, and the bank, under certain conditions, waives part of the dues. However, lenders may exercise their rights over the collateral or approach the loan’s guarantor if available. This type of closure can be detrimental to the borrower’s credit score but may be necessary under severe financial strain. - Settled Loan Closure

In a settled loan closure, the borrower is unable to clear the full outstanding amount, and the lender offers a discounted settlement. The borrower pays the reduced amount, and the remaining loan balance is waived off. While this option helps reduce debt, it can negatively impact credit scores, as “settled” status on a credit report implies the borrower could not fulfill the entire loan obligation.

Each type of loan closure has distinct implications. Preclosure and regular closure generally benefit borrowers’ credit profiles, while bad loan and settled closures can harm credit scores.

Also Read:- Apply for Pradhan Mantri Awas Yojana Online: Eligibility, Process, and Benefits

Why Do Banks Charge Foreclosure Fees?

Banks impose foreclosure charges as a way to offset the loss of future interest income. When a borrower forecloses a loan, they stop paying EMIs, which would otherwise have generated steady interest income for the lender. This fee, typically calculated as a percentage of the outstanding principal, varies by loan type, tenure, and rate (fixed or floating).

Fixed-rate home loans are more likely to incur foreclosure fees, as they guarantee a steady interest rate over the loan tenure, making early closure less favorable to banks. Conversely, floating-rate loans are less likely to carry foreclosure charges, particularly if they are home loans for individual borrowers, as per the Reserve Bank of India’s (RBI) regulatory guidelines.

Foreclosure Charges: When Do They Apply?

- Fixed-Rate Loans: Most banks charge foreclosure fees for fixed-rate loans, as these are structured with fixed interest payments.

- Dual-Rate Loans: In loans where the rate transitions from fixed to floating, charges are often applied during the fixed-rate period only.

- Business and Commercial Loans: These typically attract foreclosure charges across banks since the RBI’s protective guidelines apply only to individual borrowers.

- Car and Personal Loans: Like fixed-rate home loans, car loans also attract foreclosure charges in most cases.

While these charges are common, it’s essential to understand the situations in which they do not apply.

Home Loan Foreclosure Charges by Banks (2024)

Below is a summary of the foreclosure charges applied by various banks for home loans, categorized for individual and non-individual borrowers:

| Bank/Lender | Individual Borrowers | Non-Individual Borrowers |

|---|---|---|

| LIC Housing Finance Ltd. | 0% to 2% | 0% to 2% |

| Federal Bank | 0% to 3% | 0% to 3% |

| Dhanlaxmi Bank | 0% | As per bank terms |

| Yes Bank | 0% for floating-rate loans; 4% for fixed-rate loans | 4% on outstanding principal for fixed rates |

| ICICI Bank | 0% to 4% | 0% to 4% |

| HDFC Bank | 0% to 2% | 0% to 2% |

| SBI Bank | 0% to 3% | 0% to 3% |

This table reflects the foreclosure fee ranges as of 2024, varying by lender policies and borrower category. Individual borrowers with floating-rate loans may typically see no foreclosure charges, whereas fixed-rate loans and non-individual borrowers often incur fees. It’s recommended to confirm with the respective bank for precise terms, as rates and conditions may vary.

RBI Guidelines on Foreclosure Charges: Protection for Borrowers

In an effort to protect borrowers, the RBI has issued guidelines regarding foreclosure fees:

- Individual Floating-Rate Home Loans: The RBI mandates that banks cannot charge foreclosure fees for individual floating-rate home loans, promoting flexibility for borrowers seeking early repayment.

- Fixed-Rate Home Loans: For fixed-rate home loans, foreclosure charges may apply. However, some lenders waive these fees if the borrower uses their own funds, as opposed to a refinance from another institution.

- Business Loans: RBI guidelines do not mandate foreclosure fee exemptions for business loans, leaving the decision to individual lenders.

- Car Loans: While these are generally not covered by RBI’s foreclosure charge exemption, each bank’s policy may differ based on the borrower’s profile and tenure.

The RBI’s directives on foreclosure fees are designed to help borrowers make flexible repayment decisions. However, exemptions mainly apply to individual borrowers, meaning businesses and non-individuals generally still face foreclosure charges.

Also Read:- Best Place to Invest in Commercial Property in Mumbai.

How to Foreclose Your Home Loan?

- Notify the Lender: Start by informing your lender of your intention to foreclose.

- Prepare Documentation: Most banks will require ID proof, a foreclosure request form, and recent loan account statements.

- Settle Outstanding Dues: Pay the outstanding principal and any applicable charges to complete the foreclosure.

After closing the loan, ensure you receive a No Objection Certificate (NOC) and other closure documents from the lender. These will confirm the loan’s closure and help clear any property lien.

Benefits of Home Loan Foreclosure: Why Consider It?

- Significant Interest Savings: Foreclosing early reduces the total interest payable, saving money for long-term loans with high interest rates.

- Debt-Free Life: Clearing a large debt like a home loan reduces your monthly obligations and can provide financial freedom.

- Boosted Credit Score: Successfully foreclosing a loan boosts creditworthiness and can improve eligibility for future loans.

- Better Financial Flexibility: Without the monthly EMI burden, borrowers can focus on new investment opportunities.

Foreclosure has several financial benefits, especially for borrowers looking to enhance their credit profile or allocate funds to new projects.

Drawbacks of Home Loan Foreclosure: What to Keep in Mind

- Lump-Sum Payment Impact on Liquidity: Foreclosure requires a large upfront payment, which may affect liquidity.

- Loss of Tax Benefits: Borrowers lose tax benefits on interest paid for the remainder of the original loan tenure.

- Foreclosure Charges: The added fees may offset some of the potential interest savings, making foreclosure less financially advantageous.

Balancing the immediate savings with these drawbacks is essential to make an informed foreclosure decision.

If you’re seeking alternative ways to manage your loan burden without foreclosing, check out our blog on “Reduce EMI of Existing Home Loan – 5 Validated Tactics.”

FAQs

What is home loan foreclosure?

- Home loan foreclosure is the early repayment of the outstanding loan amount in a lump sum before the end of the loan tenure.

When is it beneficial to foreclose a home loan?

- Foreclosure is beneficial if you want to save on long-term interest costs and have surplus funds available for early repayment.

Do all banks charge foreclosure fees?

- Foreclosure charges depend on the loan type and rate. Fixed-rate loans usually have charges, while floating-rate loans for individuals may not, as per RBI guidelines.

Are foreclosure charges applicable for floating-rate home loans?

- No, RBI guidelines prohibit banks from charging foreclosure fees on floating-rate home loans for individual borrowers.

What are the types of home loan closures?

- The types include preclosure, regular closure, bad loan closure, and settled loan closure, each with specific conditions and implications.

How does foreclosure affect my tax benefits?

- Foreclosure can result in the loss of tax benefits on both principal and interest components for the remaining loan tenure.

Are there RBI guidelines on foreclosure charges for business loans?

- RBI’s foreclosure fee exemptions primarily apply to individual floating-rate home loans; business loans generally do not enjoy these exemptions.

What documents are required to foreclose a home loan?

- You typically need an ID proof, foreclosure request form, and recent loan account statements to initiate foreclosure.

Can foreclosure impact my credit score?

- Yes, foreclosure can positively impact your credit score by demonstrating your ability to clear significant debt ahead of schedule.

Are car loans subject to foreclosure charges?

- Yes, car loans often have foreclosure charges, as they are typically fixed-rate loans not covered by RBI’s no-charge directive for floating-rate home loans.

What are the pros of foreclosing a home loan?

- Benefits include savings on interest, reduced debt burden, financial flexibility, and a positive effect on credit scores.

What are the cons of foreclosing a home loan?

- Potential drawbacks include a significant impact on liquidity, loss of tax benefits, and possible foreclosure charges.

What is the difference between preclosure and regular closure?

- Preclosure is the early repayment of the loan, while regular closure involves paying off the loan according to the original tenure and EMI schedule.

What is a settled loan closure, and how does it affect credit?

- A settled loan closure involves paying a negotiated, reduced amount, and it may negatively impact your credit score as it indicates you could not meet the full loan obligations.

Can I foreclose my loan using borrowed funds?

- Some banks charge higher foreclosure fees if funds come from a refinance loan; check with your lender about their policy.

What are the foreclosure charges for fixed-rate home loans?

- Fixed-rate home loans typically attract foreclosure fees, usually a percentage of the outstanding principal, though some lenders may waive fees under specific conditions.

How can I avoid foreclosure charges?

- Opt for a floating-rate home loan (for individuals), as RBI prohibits foreclosure fees on these. Also, using personal funds rather than refinancing can help avoid higher fees.

Can foreclosure save me money in the long term?

- Yes, by closing a loan early, you can save substantial interest, especially on long-term loans with high-interest rates.

Does RBI have guidelines on foreclosure charges for car loans?

- RBI’s guidelines on foreclosure charge exemptions apply primarily to individual floating-rate home loans, so car loans typically incur charges.

What happens if I foreclose only part of my loan?

- Partial foreclosure reduces the principal and can lower the EMIs or shorten the tenure, depending on the lender’s policies.

Post navigation

Previous Post

Michael Clark wins hero world hard Dirt Race10

Michael Clark wins hero world hard Dirt Race10