The Union Budget 2024 has introduced pivotal changes to the taxation of inherited property, specifically in the realm of long-term capital gains (LTCG). These changes, aimed at simplifying the tax process, have far-reaching implications for taxpayers, especially those dealing with inherited properties. This guide explores the updated tax regulations in depth, offering a thorough understanding of how these changes will affect you, along with practical advice for minimizing tax liabilities.

Introduction to Inherited Property and Capital Gains

Inheritance in India involves the transfer of assets, including immovable property, from the deceased to their legal heirs. While India does not impose an inheritance tax or estate duty (abolished in 1985), the sale of inherited property triggers capital gains tax. Understanding the taxation of these gains is crucial for anyone dealing with inherited real estate.

Key Terms:

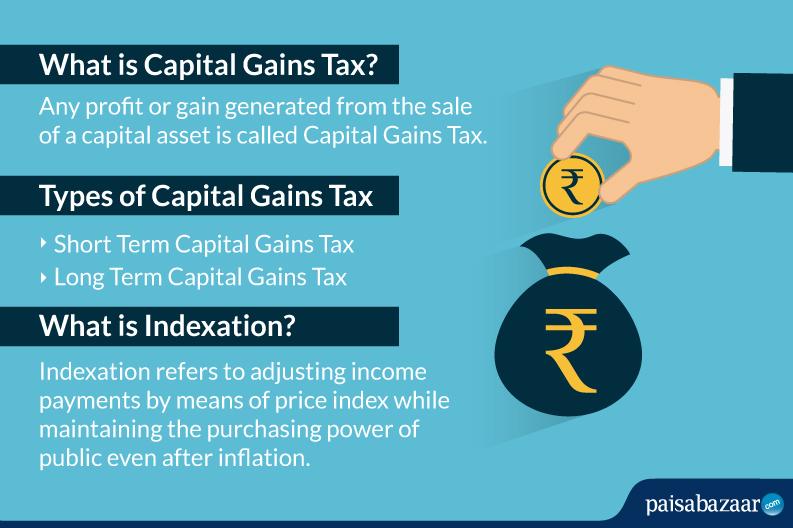

- Capital Gains Tax: A tax levied on the profit realized from the sale of an asset.

- Long-Term Capital Gains (LTCG): Gains from the sale of an asset held for more than 24 months.

- Short-Term Capital Gains (STCG): Gains from the sale of an asset held for 24 months or less.

Inherited property, when sold, is generally subject to LTCG tax since it is usually held for an extended period before the sale. The tax is calculated on the difference between the sale price and the cost of acquisition, with certain adjustments allowed under previous tax rules.

2. Major Changes Introduced in Budget 2024

The Budget 2024 brought two significant amendments to the taxation of LTCG from the sale of real estate:

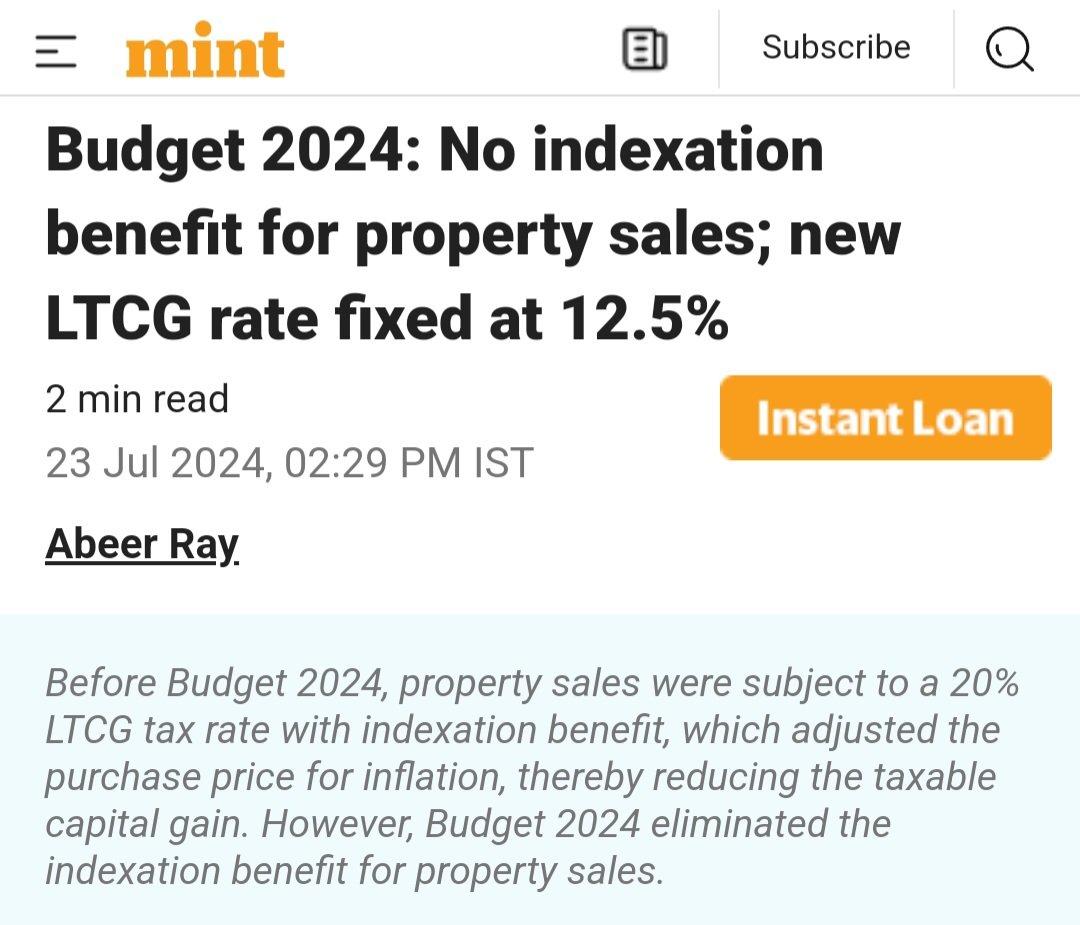

Image: The Mint

- Elimination of the Indexation Benefit:

- Previous Regime: Prior to Budget 2024, taxpayers could use the Cost Inflation Index (CII) to adjust the purchase price of the property for inflation. This indexation significantly reduced the taxable capital gain by increasing the cost base of the property.

- Current Regime: Post-Budget 2024, the indexation benefit has been removed. Taxpayers can no longer adjust the purchase price for inflation, which often results in a higher taxable gain.

- Reduction in LTCG Tax Rate:

- Previous Rate: The LTCG tax rate on real estate was 20%.

- Current Rate: The LTCG tax rate has been reduced to 12.5%. While the rate cut seems favorable, the removal of the indexation benefit means that the effective tax burden may still be higher for many taxpayers.

Impact Analysis:

- Pre-Budget Scenario: A property purchased in 1995 for ₹10 lakh and sold in 2024 for ₹1 crore could have been indexed to a higher acquisition cost, say ₹40 lakh, reducing the taxable gain to ₹60 lakh. The tax payable would be ₹12 lakh (20% of ₹60 lakh).

- Post-Budget Scenario: Without indexation, the taxable gain is ₹90 lakh, and the tax payable is ₹11.25 lakh (12.5% of ₹90 lakh). Though the tax rate is lower, the higher taxable gain due to the removal of indexation can result in a comparable or higher tax outlay.

These changes highlight the government’s attempt to streamline the taxation process while maintaining a significant tax revenue stream.

Detailed Breakdown of Taxation on Inherited Property

When you inherit a property, the acquisition cost for capital gains tax calculation is determined based on when the original owner (the deceased) purchased the property.

Scenarios:

- Property Acquired Before April 1, 2001:

- Fair Market Value (FMV) Method: The FMV of the property as of April 1, 2001, is considered as the cost of acquisition. Earlier, this value could be indexed to account for inflation, reducing the taxable gain.

- Post-Budget: The FMV remains the acquisition cost, but without indexation, the gap between the FMV and the sale price is fully taxable.

- Property Acquired After April 1, 2001:

- Actual Purchase Price: The original purchase price is used as the cost of acquisition. With the removal of indexation, the full difference between this cost and the sale price is subject to LTCG tax.

Example:

- Consider a property purchased in 1998 for ₹20 lakh. Its FMV in 2001 was ₹30 lakh, and it is sold in 2024 for ₹1.5 crore.

- Pre-Budget 2024 Calculation: Indexed cost = ₹30 lakh * (CII for 2024 / CII for 2001) = ₹90 lakh (approx). Taxable gain = ₹1.5 crore – ₹90 lakh = ₹60 lakh. Tax = ₹60 lakh * 20% = ₹12 lakh.

- Post-Budget 2024 Calculation: Cost of acquisition = ₹30 lakh (No indexation). Taxable gain = ₹1.5 crore – ₹30 lakh = ₹1.2 crore. Tax = ₹1.2 crore * 12.5% = ₹15 lakh.

This example illustrates that while the tax rate has decreased, the removal of indexation can result in a higher overall tax liability.

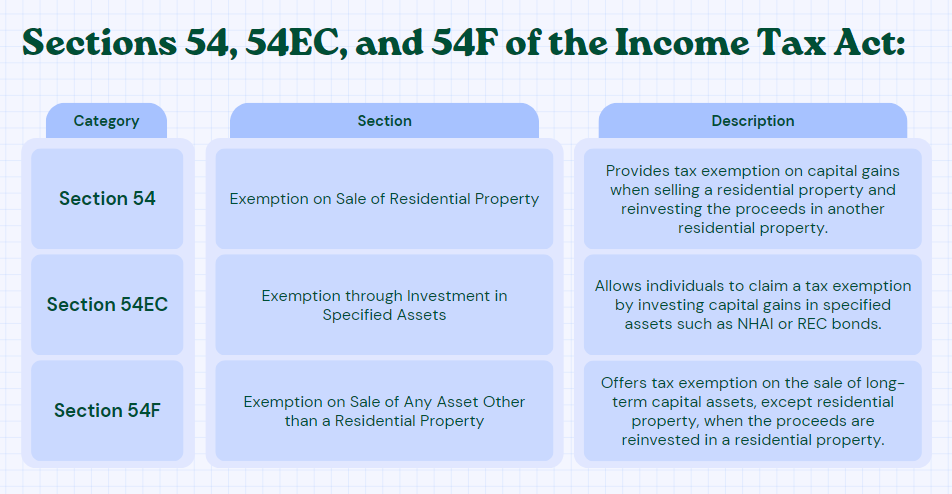

Exemptions Available Under Sections 54 and 54EC

To mitigate the impact of capital gains tax, the Income Tax Act offers exemptions under certain conditions:

- Section 54:

- Exempts LTCG if the proceeds are reinvested in purchasing or constructing another residential property within a specified time frame.

- Conditions: The new property must be purchased within two years or constructed within three years from the sale date of the original property.

- Section 54EC:

- Allows exemption if the gains are invested in specified bonds (e.g., NHAI, REC) within six months from the date of sale.

- Lock-In Period: The investment must be held for five years to avail the exemption.

Strategic Use:

- Reinvestment Strategy: If the gains are substantial, reinvesting in a new property or bonds can significantly reduce the tax liability. For instance, investing ₹1 crore in bonds under Section 54EC could save up to ₹12.5 lakh in taxes.

New Considerations Post-Budget 2024:

- Given the increased taxable amount due to the removal of indexation, leveraging these exemptions becomes even more critical for taxpayers looking to optimize their tax liabilities.

Practical Implications and Tax Planning

Navigating the complexities of inherited property taxation under the new rules requires careful planning:

- Assessing Market Conditions: Consider the timing of the sale. If the real estate market is favorable, the benefits of selling might outweigh the higher tax liability.

- Reinvestment Decisions: Weigh the options of reinvesting in another property or bonds. Given the stricter timelines for reinvestment, advance planning is crucial.

- Consultation with Experts: Given the complexities of the new tax regime, it is advisable to consult with a tax professional or financial advisor to develop a tax-efficient strategy.

Case Study:

- Scenario: A taxpayer inherited a commercial property in 2005 valued at ₹50 lakh at the time of inheritance. The property is now worth ₹3 crore.

- Tax Implications: Under the new rules, without indexation, the entire difference between ₹50 lakh and ₹3 crore will be taxable at 12.5%, leading to a significant tax outlay.

- Strategy: To minimize tax, the taxpayer might consider reinvesting the gains under Section 54 or 54EC, potentially saving lakhs in taxes.

6. Key Considerations for Property Owners Post-Budget 2024

Impact of Removal of Indexation:

- Older Properties: The removal of indexation primarily affects properties acquired before 2001, as these properties could previously benefit from substantial inflation adjustments.

- Younger Properties: For properties acquired after 2001, the absence of indexation, combined with the reduced tax rate, could still result in a heavier tax burden due to the larger unadjusted gains.

Real Estate Market Dynamics:

- Holding vs. Selling: Property owners need to consider whether it’s better to hold onto the property or sell. Market conditions, potential appreciation, and the tax implications of selling under the new regime should all factor into this decision.

- Estate Planning: Individuals might also consider estate planning tools like gifts, trusts, or wills to manage the transfer of property in a tax-efficient manner.

7. Conclusion

The Union Budget 2024 has significantly altered the landscape of property taxation in India, particularly for those dealing with inherited real estate. The removal of indexation benefits, coupled with a reduction in LTCG tax rates, can result in a higher tax burden for many taxpayers. Understanding these changes and strategically planning property sales and reinvestments are crucial for minimizing tax liabilities.

For those inheriting property, it’s essential to stay informed about the latest tax regulations and consult with experts to navigate this complex terrain effectively.

FAQs

What is the new LTCG tax rate on inherited property sales post-Budget 2024?

- The LTCG tax rate on the sale of inherited property has been reduced to 12.5%.

Can I still claim indexation benefits on inherited property?

- No, the indexation benefit has been removed for properties sold after April 2024.

How is the acquisition cost determined for inherited property?

- For properties acquired before April 1, 2001, the FMV as of April 1, 2001, is used as the acquisition value as of April 1, 2001. For properties acquired after that date, the original purchase price is used.

What if the inherited property was purchased after April 1, 2001?

- The acquisition cost will be the actual price paid by the original owner. Since indexation is no longer applicable, the taxable gain will be the difference between the sale price and this acquisition cost.

Can I reinvest the sale proceeds to avoid paying LTCG tax?

- Yes, you can reinvest the sale proceeds under Section 54 (in residential property) or Section 54EC (in specified bonds) to claim an exemption from LTCG tax.

What are the deadlines for reinvestment under Section 54 and Section 54EC?

- For Section 54, you must reinvest in a new residential property within two years (purchase) or three years (construction). For Section 54EC, you must invest in specified bonds within six months of the sale.

Is there any advantage to holding onto the property longer under the new tax rules?

- Holding the property could be beneficial if you expect significant appreciation in value. However, consider the potential tax burden when selling under the new rules.

How does the removal of indexation affect the sale of older properties?

- The removal of indexation primarily affects older properties acquired before April 1, 2001, as these properties could previously benefit from inflation adjustments that reduced taxable gains.

What strategies can be used to minimize tax on inherited property sales?

- Strategies include timing the sale to optimize market conditions, reinvesting in new properties or bonds, and consulting with tax professionals to explore other tax-efficient options.

Is the reduced LTCG tax rate a positive change for all taxpayers?

- The reduced LTCG tax rate is beneficial for some taxpayers, but the removal of indexation can lead to a higher effective tax burden, particularly for those selling long-held properties.

Also Read:- Rising Demand of Luxury Living In India Your Guide to Luxury Living

Post navigation

Previous Post

Michael Clark wins hero world hard Dirt Race10

Michael Clark wins hero world hard Dirt Race10