Introduction

Owning a home is a dream for many, but the financial commitment it requires can be daunting. Most homeowners take on long-term home loans, with tenures stretching up to 20 or 30 years. While this provides manageable monthly payments, it also means paying a significant amount in interest over time. The question is: how can you reduce the loan tenure and become debt-free sooner without straining your finances?

Reducing your home loan tenure is about making smart financial decisions that allow you to pay off your loan faster, saving both time and money. This guide will dive deep into five validated tactics for reducing your loan tenure. Each tactic addresses key questions, providing a roadmap to help you reach your goal of full home ownership faster. Whether you’re looking to make lump-sum payments, adjust your EMI, or refinance, this guide offers actionable insights to help you navigate these choices confidently.

Also Read:- Best Place to Invest in Commercial Property in Mumbai

Can Increasing Your EMI Reduce Your Loan Tenure?

Increasing your Equated Monthly Installment (EMI) is one of the most straightforward ways to reduce your loan tenure. By paying more each month, you reduce the principal balance faster, which in turn decreases the amount of interest you’ll pay over the loan term. Here’s how it works and why it’s effective.

Detailed Example:

Imagine you have a 20-year home loan of ₹50 lakhs with an interest rate of 7%. Your initial EMI is around ₹38,765. If you increase this EMI by just 10% to ₹42,641, you’ll reduce your loan tenure by nearly 3 years, paying off the loan in about 17 years. Additionally, you’d save around ₹6 lakhs in interest.

How to Implement This Strategy:

- Calculate Affordability: Use an EMI calculator to determine the maximum EMI you can afford. Ensure it’s within your budget and doesn’t strain your finances.

- Contact Your Lender: Request an EMI increase. Many banks allow borrowers to adjust EMI annually, often in alignment with salary increments.

- Review Annually: Make it a habit to assess your finances yearly. Any additional increment or bonus can help boost your EMI further, shaving even more time off your loan.

Benefits:

- Lower Interest Payments: A higher EMI reduces the principal faster, lowering the total interest you pay over the loan term.

- Debt-Free Sooner: Paying a little extra each month means fewer years of loan repayments and more financial freedom sooner.

- Should You Make Regular Part-Payments?

Periodic part-payments can be a powerful way to reduce your loan tenure, particularly if you have irregular sources of income, like annual bonuses, tax refunds, or investment gains. When you make part-payments, the lump sum goes directly towards the principal, significantly lowering the outstanding balance and thereby reducing the interest burden.

Detailed Example:

Let’s say you have the same ₹50 lakh loan at 7% interest over 20 years. By making an annual part-payment of ₹2 lakhs from bonuses or savings, you could reduce your loan tenure by almost 6 years, cutting down the interest by about ₹10 lakhs.

How to Implement This Strategy:

- Set a Target: Aim to make part-payments during financially favorable times, such as after bonuses or tax refunds. Even one-time part-payments can make a noticeable difference.

- Check for Penalties: Some lenders charge fees on part-payments for fixed-rate loans. Be clear on the terms before making payments.

- Calculate the Impact: Use a loan tenure calculator to see how a part-payment of ₹1 lakh, ₹2 lakh, or more affects your tenure and interest.

Benefits:

- Directly Reduces Principal: Part payments reduce your principal balance, which decreases the interest portion of your EMI, allowing more of your EMI to go towards the principal.

- Flexible Payment: Part payments don’t require a fixed commitment; they’re flexible, allowing you to contribute whenever possible.

Also Read:- Best Sleeping Directions As Per Vastu

Can Opting for a Loan Tenure Reduction Work When Refinancing?

Refinancing, or transferring your home loan to a new lender with lower interest rates, is an option worth considering, especially if interest rates have dropped significantly since you took the loan. Beyond interest savings, refinancing allows you to reduce the loan tenure by keeping the EMI the same while shortening the term, speeding up repayment.

Detailed Example:

Suppose your current loan is at 8%, and you find a lender offering 6.5%. By refinancing, you can keep the same EMI but reduce the loan tenure by a few years. For instance, a 20-year loan could be paid off in 17 years, saving both time and considerable interest.

How to Implement This Strategy:

- Shop for Lower Rates: Explore competitive interest rates among different banks and housing finance companies. Even a 0.5% reduction can lead to substantial savings.

- Evaluate Transfer Costs: Refinancing may involve fees for processing and administrative costs. Ensure the overall savings justify the transfer expenses.

- Discuss Tenure Reduction: When refinancing, talk to the lender about maintaining your EMI but reducing the loan tenure. This approach accelerates your repayment and cuts down on total interest.

Benefits:

- Shorter Loan Tenure: Refinancing with a reduced tenure means you’ll be debt-free sooner, even if the EMI remains the same.

- Interest Savings: A lower rate combined with a shorter tenure leads to substantial interest savings, leaving more money for other goals.

How Does Switching to a Higher EMI Plan Help?

Certain lenders offer flexible EMI plans, allowing borrowers to gradually increase their EMI as their income grows. Known as step-up EMIs, these options can be highly beneficial if you’re confident in your income growth, such as a predictable salary increase over the years. This allows you to put more towards the principal over time, reducing tenure without immediately affecting your budget.

Detailed Example:

Imagine starting with a ₹50 lakh loan with an initial EMI of ₹35,000. By choosing a step-up plan, you could increase your EMI by 5% every two years. This adjustment can reduce your loan tenure by several years, significantly lowering the interest paid.

How to Implement This Strategy:

- Ask Your Bank: Not all banks offer step-up EMIs. If yours does, discuss the terms and frequency of EMI increases.

- Align with Career Growth: Since income often grows incrementally, a step-up EMI option aligns well with anticipated salary increments.

- Review Regularly: Revisit your EMI annually or every few years. If your financial situation improves, increasing the EMI can reduce the loan tenure further.

Benefits:

- Balances Income Growth and Repayment: A step-up EMI adapts to your income, making it more affordable.

- Reduces Total Interest: Since a larger EMI means more goes toward the principal, interest decreases over time.

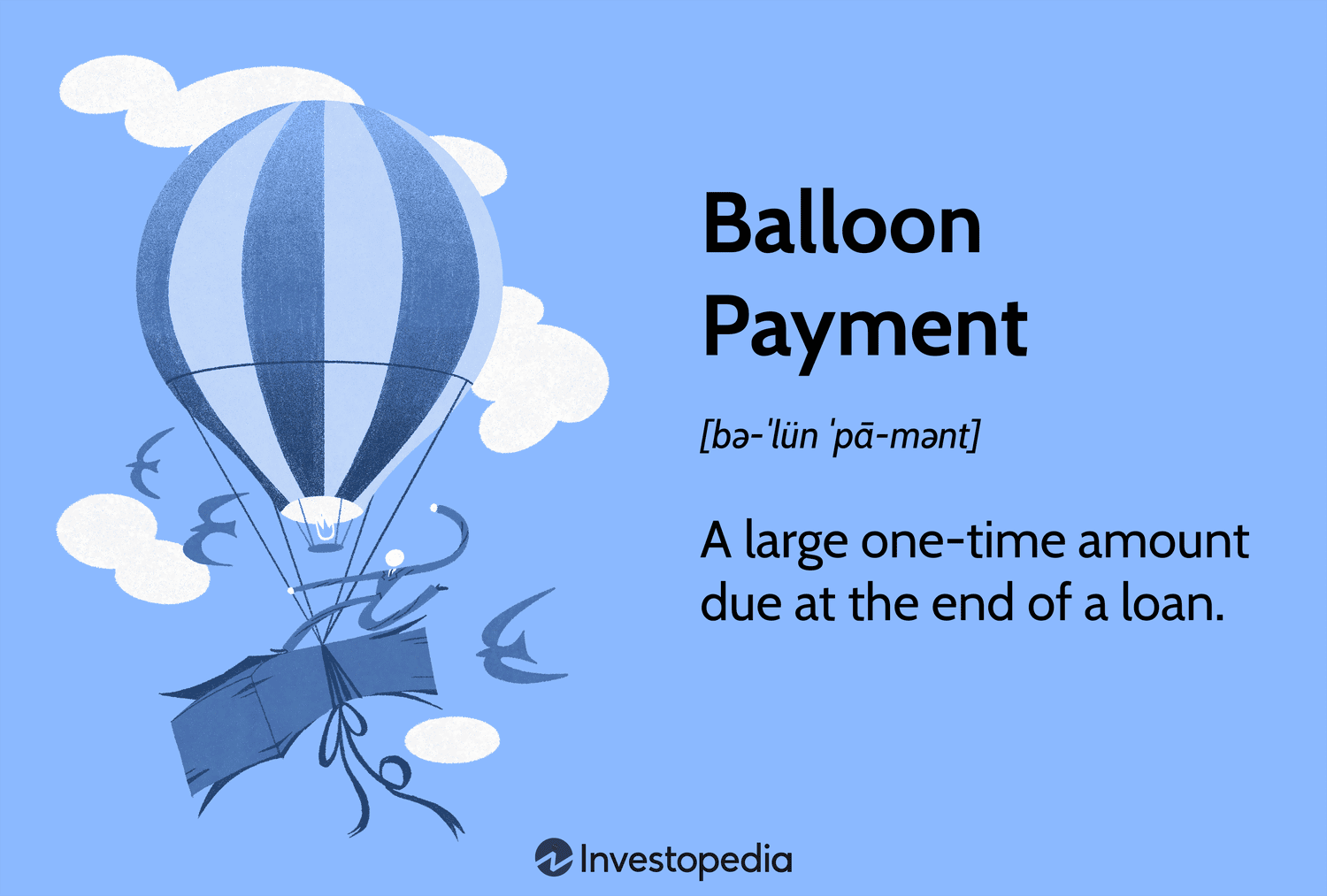

Can a Loan Restructure with a Balloon Payment Reduce Tenure?

A balloon payment involves making a substantial one-time payment toward the loan principal. Traditionally, balloon payments are made at the end of the loan term, but if feasible, making this payment earlier can help reduce the loan tenure by several years. It’s a viable option for those who might receive large sums at predictable intervals.

Detailed Example:

If you have a ₹50 lakh loan and make a balloon payment of ₹5 lakhs midway through the tenure, you could reduce your tenure by a few years, depending on the EMI amount. This not only shortens the term but also brings down the overall interest cost substantially.

How to Implement This Strategy:

- Plan for the Payment: Set aside funds over time or allocate windfalls like inheritances, dividends, or investment returns for a balloon payment.

- Negotiate with Lender: Check if your lender allows early balloon payments and if they charge any fees.

- Evaluate Financial Impact: Determine how a balloon payment will affect your cash flow and overall finances.

Benefits:

- Drastic Reduction in Tenure: Balloon payments significantly reduce the principal, bringing down both tenure and interest.

- More Flexibility: This strategy doesn’t affect your regular EMI, making it suitable for those with periodic lump-sum income.

Conclusion

Reducing your home loan tenure is achievable with a few smart financial decisions. By increasing EMIs, making periodic part-payments, refinancing at a lower interest rate, opting for a step-up plan, or making a balloon payment, you can accelerate loan repayment and save on interest costs. Each of these strategies offers distinct benefits, allowing you to tailor your approach based on your financial situation. The ultimate goal is to pay off your loan sooner, giving you peace of mind and more freedom to pursue other financial goals. So, take control of your home loan today, and make your journey to debt-free homeownership a reality!

FAQs

Can I increase my EMI anytime?

- Yes, many banks allow it; check for terms with your lender.

What is a part-payment?

- It’s a lump-sum payment made periodically to reduce the loan principal.

Is refinancing always beneficial?

- Only if the new interest rate and tenure offer cost savings after fees.

Are there penalties for part-payments?

- Some banks charge fees, especially on fixed-rate loans.

What is a balloon payment?

- A large payment made at the loan’s end to reduce the principal and interest.

Can I reduce my EMI and tenure simultaneously?

- No, usually you’ll choose one – either lower EMI or shorter tenure.

Does increasing EMI reduce my interest?

- Yes, as more goes toward the principal, lowering overall interest.

What’s the best time to make part-payments?

- Early in the loan tenure to maximize interest savings.

Is tenure reduction possible without refinancing?

- Yes, by increasing EMI or making part-payments.

Do all banks offer flexible EMI plans?

- No, check with your lender for available options.

How often can I switch to a higher EMI?

- Most banks allow an annual or bi-annual review for EMI adjustments.

Is refinancing difficult to process?

- It involves paperwork and fees, but can be worthwhile.

Can I switch lenders more than once?

- Yes, but multiple switches may incur additional fees and checks.

Does tenure reduction affect my credit score?

- It usually has a positive effect due to reduced debt.

Can I refinance with a longer tenure?

- Yes, though it increases interest costs.

Are part-payments better than EMI increase?

- Part-payments may save more, especially early in the loan term.

Does a balloon payment affect EMI?

- It can reduce EMI if applied during the loan term.

What documents are needed for refinancing?

- Typically, ID proof, loan statements, and income proof.

Can I make part-payments online?

- Many banks offer online part-payment options; check with your lender.

What’s a tenure reduction option in refinancing?

- Choosing to keep EMI the same while reducing the repayment period.

Post navigation

Previous Post

Michael Clark wins hero world hard Dirt Race10

Michael Clark wins hero world hard Dirt Race10